Why EN590 Diesel Remains Central in a Changing Energy World

Despite the relentless march toward electrification and renewable energy, Ultra-Low Sulfur Diesel (ULSD) meeting EN590 specifications remains a linchpin of the global energy system. From powering heavy-duty trucks and construction equipment to fueling backup generators and supporting agricultural machinery, EN590 diesel’s unique blend of performance, emissions control, and compatibility with modern engines ensures its continued relevance. As we look ahead to the next 5–10 years, the market for EN590 diesel is being shaped by a complex interplay of regulatory tightening, technological innovation, shifting regional demand, and the rise of alternative fuels. This report explores these dynamics in depth, providing actionable insights for refiners, traders, distributors, and policymakers navigating the evolving landscape of ULSD EN590 demand.

Contact Us

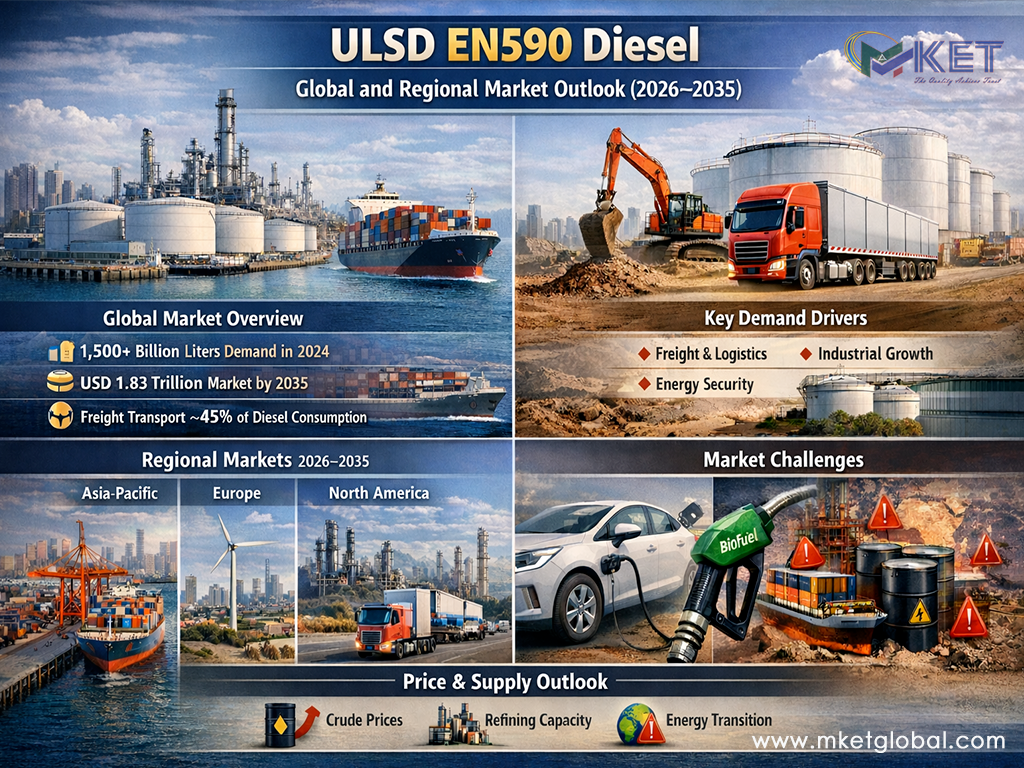

1. Global Demand Outlook for ULSD EN590 Diesel (2026–2035)

1.1. Market Size and Growth Trajectory

The global diesel market—valued at approximately $1.16 trillion in 2025—is projected to grow steadily, reaching $1.78 trillion by 2035, with a compound annual growth rate (CAGR) of 4.4%. While this encompasses all diesel grades, EN590-compliant ULSD constitutes the dominant share in Europe and is increasingly the benchmark for international trade, especially in regions with tightening emissions standards.

Key drivers of demand include:

- Heavy-duty transportation (trucking, shipping, rail)

- Construction and infrastructure development

- Industrial and mining operations

- Agricultural machinery and off-grid power generation

Despite the rise of electric vehicles (EVs) and alternative fuels, over 72% of global commercial vehicles and 61% of heavy machinery are still powered by diesel, with a growing share using ULSD. The transition to cleaner fuels is most pronounced in developed economies, but emerging markets continue to rely heavily on diesel for economic growth and infrastructure expansion.

1.2. Shifting Regional Patterns

The next decade will see a geographic rebalancing of EN590 diesel demand:

- Mature economies (Europe, parts of North America) will see flat or declining demand due to efficiency gains, electrification, and modal shifts.

- Developing regions (Asia-Pacific, Africa, Middle East) will drive incremental growth, underpinned by industrialization, urbanization, and logistics expansion.

Table 1: Regional Share of Global Diesel Demand (2025 vs. 2035, All Grades)

| Region | 2025 Share (%) | 2035 Share (%) | Key Trends |

| Asia-Pacific | 41 | 44 | Industrial/logistics growth, urbanization |

| Europe | 27 | 22 | Efficiency, alternative fuels, import focus |

| North America | 21 | 18 | Freight, slow electrification, renewables |

| Middle East/Africa | 11 | 16 | Infrastructure, power, logistics, imports |

Source: Global Growth Insights, Data Insights Market, Exporters Worlds, S&P Global Commodity Insights

The table highlights the relative decline in Europe and North America’s share as Asia-Pacific and Africa increase their consumption, reflecting both economic growth and slower adoption of alternatives in emerging markets.

2. Europe: Regulatory Developments and Policy Drivers

2.1. EN590 Specification and Compliance

EN590 is the European standard for automotive diesel, mandating a maximum sulfur content of 10 ppm, a minimum cetane number of 51, and strict density and cold flow properties. Compliance is non-negotiable for market access, with buyers demanding rigorous documentation and traceability.

Key compliance requirements:

- Certificates of Analysis (COA) for each batch

- Independent laboratory testing

- Sustainability declarations for biodiesel components

- Full traceability and origin documentation

Non-compliance can result in severe penalties, shipment rejection, and reputational damage.

2.2. Environmental Policy and Renewable Mandates

Europe’s environmental policy is the most aggressive globally, with the European Green Deal targeting a 55% reduction in emissions by 2030 and net-zero by 2050. The Renewable Energy Directive (RED III), effective since 2023, mandates:

- At least 42.5% of final energy consumption from renewables by 2030

- 29% renewable share in transport or a 14.5% reduction in emissions intensity

- Minimum 5.5% advanced biofuels/hydrogen in transport

- Biodiesel blending mandates: B7 (7% FAME) is standard, with B10 and higher blends expanding

Table 2: Selected EU Member State Biofuel Mandates (2025)

| Country | Biofuel in Diesel (%) | Advanced Biofuel Target (%) | GHG Intensity Reduction (%) |

| France | 9.4 | 0.7 | -10 |

| Germany | — | 0.7 | -10.6 |

| Italy | — | 9.0 (HVO) | -6 |

| Poland | 5.2 | 0.1 | — |

| Spain | — | 1.0 | -6 |

Source: ePURE, Swiss Biofuels Association, RED III, national policies

Implications:

- Rising biodiesel content (B10 and above) is likely, especially in France, Germany, and Italy.

- Feedstock sustainability and traceability are critical, with double-counting for waste-based biofuels (UCOME, TME).

- Winter-grade diesel (CFPP -15°C or lower) commands seasonal premiums.

2.3. Market Dynamics and Import Dependency

Europe is structurally import-dependent for EN590 diesel due to:

- Declining domestic refinery capacity (closures, conversions to biofuels)

- Stringent environmental regulations increasing compliance costs

- Geopolitical disruptions (Russian sanctions, Middle East tensions)

Key import sources: Middle East, US Gulf Coast, India, and, increasingly, North Africa and West Africa (Dangote refinery).

Market pricing: Rotterdam and ARA (Amsterdam-Rotterdam-Antwerp) serve as the main benchmarks, with EN590 trading at a premium of $15–30/MT over standard diesel, and additional premiums for winter grades and full documentation.

2.4. Strategic Outlook

Europe’s EN590 diesel market will remain robust but increasingly competitive and compliance-driven. Exporters must:

- Demonstrate full specification adherence and documentation

- Adapt to rising biodiesel mandates and feedstock scrutiny

- Manage logistics and supply chain risks amid tight inventories and geopolitical volatility

3. Asia: Regional Trends and Key Markets

3.1. India: Rapid Growth and Refinery Expansion

India is poised to be the world’s largest driver of diesel demand growth by 2030. According to the International Energy Agency (IEA):

- Diesel demand will rise from 1.8 million barrels/day (2023) to 2.3 million barrels/day (2030), a 4.5% annual increase

- Diesel will account for nearly half of India’s total oil demand growth

- Commercial trucking, infrastructure, and public transport are the main drivers

Refinery capacity is expanding rapidly:

- Major projects by Indian Oil Corporation (IOC), BPCL, HPCL, and others will add millions of tons of new capacity by 2030

- IOC plans to export 4–5 million tons of diesel annually from 2027, targeting regional and global markets

Biodiesel blending and alternative fuels are growing but remain limited by feedstock availability and cost.

3.2. China: Transition and Policy Shifts

China’s diesel demand is stabilizing as the economy matures and electrification accelerates in urban transport. However:

- Heavy-duty trucking, construction, and rural/agricultural sectors remain diesel-dependent

- Refinery upgrades and new capacity (including export-oriented “teapot” refineries) are focused on producing EN590-compliant ULSD for both domestic and export markets

China is also investing in renewable diesel and hydrogen for long-term decarbonization, but these remain at an early stage.

3.3. Southeast Asia: Import Reliance and Infrastructure

Southeast Asia is a diverse, price-sensitive market:

- Industrial expansion, e-commerce logistics, and urbanization sustain diesel demand

- Many countries (e.g., Indonesia, Vietnam, Philippines) lack sufficient refining capacity and rely on imports of EN590 diesel, especially for urban fleets and export industries

- Biodiesel blending mandates (notably in Indonesia and Malaysia) are rising, but EN590 remains the standard for international trade and high-performance applications

Exporters targeting Asia must understand local procurement cycles, pricing behavior, and regulatory nuances.

4. Africa: Infrastructure, Refining Capacity, and Import Dependence

4.1. Diesel as the Economic Backbone

Across Africa, diesel is the heartbeat of economies—powering trucks, buses, mining, agriculture, and backup generators. Diesel price shifts ripple through food security, SME survival, and industrial competitiveness.

Key facts:

- Africa’s diesel prices are among the world’s lowest, due to subsidies and resource wealth (e.g., Libya, Algeria, Egypt)

- Many countries lack sufficient refining capacity, making them structurally import-dependent

- Diesel is critical for food supply chains, public transport, and energy security

4.2. Refinery Developments: The Dangote Effect

The Dangote Petroleum Refinery in Nigeria (650,000 barrels/day) is a game-changer:

- Has ended West Africa’s dependence on imported diesel and jet fuel, now exporting to neighboring countries and global markets (US, Saudi Arabia)

- Nigeria’s fuel imports dropped from 500,000 barrels/day (2023) to 88,000 (Q1 2025)

- Regional crude throughput rose nearly 78% year-on-year in 2024, almost entirely due to Dangote

Other African regions (East, Southern Africa) remain heavily import-dependent, with limited refining upgrades.

4.3. Risks and Opportunities

Benefits of low diesel prices:

- Stabilize food prices, support SMEs, and enhance industrial competitiveness

- Enable intra-African trade under the African Continental Free Trade Area (AfCFTA)

Risks:

- Fiscal pressure from subsidies

- Delayed transition to renewables

- Vulnerability to global supply disruptions and price shocks

Exporters and traders must tailor offerings to Africa’s unique mix of price sensitivity, volume flexibility, and logistical challenges.

5. Refinery Capacity and Upgrades for EN590 ULSD

5.1. Global Refining Trends

Refinery closures and rationalization in mature markets (Europe, North America) have tightened supply, while new capacity is coming online in Asia, the Middle East, and Africa.

Key developments:

- Middle East and Indian refineries are investing in advanced hydrodesulfurization (HDS) and deep HDS units to meet EN590 standards

- US Gulf Coast refineries are increasing exports to Europe and Latin America, leveraging flexible configurations

- African capacity is expanding (Dangote), but many regions still lack sufficient domestic production

5.2. Technological Advancements

Modern refinery technologies for ULSD production include:

- Hydrodesulfurization (HDS): Reduces sulfur from 50–500 ppm to <10 ppm

- Isotherm Ing® hydro-processing: Enables efficient LCO (light cycle oil) upgrading to ULSD, with lower operating costs and longer catalyst life

- Isomerization: Improves cold flow properties while maintaining cetane number

Refineries lacking these capabilities face competitive disadvantages, especially when targeting Europe or other regulated markets.

5.3. Investment and Capex Trends

Major oil companies (BP, Shell, ExxonMobil, Sinopec, Indian Oil, TotalEnergies, Chevron, Petronas) are investing in:

- Refinery upgrades for ULSD and renewable diesel production

- Blending infrastructure for biodiesel and HVO

- Digitalization and automation for quality control and traceability

India, the Middle East, and the US are leading in new capacity and export-oriented investments.

6. Alternative Fuels and Competition

6.1. Renewable Diesel, HVO, and E-Diesel

Renewable diesel (HVO) and e-diesel are gaining momentum, especially in Europe:

- HVO can be used as a drop-in replacement for EN590 diesel, enabling immediate CO₂ reductions without engine modifications

- Germany, the Netherlands, Italy, and France are translating RED III targets into national law, boosting HVO demand

- E-diesel (synthetic fuels from renewable electricity and CO₂) is in early commercialization, with potential for long-term decarbonization

Feedstock availability and cost remain constraints, with waste-based and advanced biofuels prioritized for sustainability.

6.2. Biodiesel Blending Mandates

Biodiesel (FAME) blending is standard in Europe (B7), with B10 and higher blends expanding. Some countries (Italy, Sweden) have specific mandates for HVO or advanced biofuels.

Operational considerations:

- Storage compatibility (water absorption, microbial growth)

- Cold flow properties (cloud point, CFPP)

- Quality degradation (oxidation, shelf life)

Feedstock sustainability and traceability are critical for compliance with RED III and national mandates.

6.3. LNG, Electrification, and Hydrogen

LNG is gaining share in shipping and some heavy-duty transport, especially in Asia and Europe, but infrastructure and cost remain barriers.

Electrification is advancing in passenger vehicles and urban fleets but has limited penetration in heavy-duty, long-haul, and off-grid applications.

Hydrogen (fuel cells, H2-ICE) is being piloted in heavy trucks (notably in India and China), but widespread adoption is a decade away.

7. Transportation Sector Shifts: Trucking, Shipping, Rail, and Construction

7.1. Trucking and Logistics

Heavy-duty trucking remains the largest consumer of EN590 diesel globally:

- Over 72% of global commercial vehicles are diesel-powered

- Infrastructure development and e-commerce logistics are sustaining demand, especially in Asia and Africa

- Fleet renewal and efficiency gains are slowing demand growth in Europe and North America

Hydrogen and electric trucks are emerging but will not displace diesel at scale before 2035.

7.2. Shipping: IMO Regulations and Marine Fuels

The International Maritime Organization (IMO) has approved net-zero regulations for global shipping, targeting:

- Net-zero GHG emissions by 2050

- Mandatory marine fuel standards and GHG pricing from 2027/2028

Implications:

- Shift toward very low sulfur fuel oil (VLSFO), marine gasoil (MGO), and alternative fuels (LNG, methanol, ammonia)

- EN590 diesel remains relevant for smaller vessels, auxiliary engines, and as a blending component

- Shipping sector’s transition will gradually reduce diesel demand, but not eliminate it in the next decade

7.3. Rail and Construction

Railways in emerging markets (India, Africa, Southeast Asia) continue to rely on diesel locomotives, with electrification progressing slowly.

Construction and mining are major diesel consumers, especially in regions with large infrastructure pipelines (Asia, Africa, Middle East).

8. Market Pricing, Premiums, and Trading Dynamics

8.1. Benchmarks and Price Formation

EN590 diesel is priced against major benchmarks:

- Rotterdam/ARA (Amsterdam-Rotterdam-Antwerp): Primary European benchmark, with daily assessments by S&P Global Platts, CME Group, and others

- US Gulf Coast, Singapore, Fujairah: Key export hubs for global trade

Premiums and differentials:

- EN590 ULSD typically trades at a $15–30/MT premium over standard diesel

- Additional premiums for winter grades, full documentation, and traceability

- Biodiesel-blended grades (B7, B10) have separate pricing, reflecting feedstock costs and sustainability certification

8.2. Price Volatility and Supply Chain Risks

Price volatility is driven by:

- Crude oil price swings

- Refining margins and outages (planned/unplanned)

- Geopolitical disruptions (sanctions, conflicts, shipping risks)

- Currency fluctuations and freight rates

Recent trends:

- Tightening supply in Europe and the Atlantic Basin due to Russian sanctions, Middle East outages, and refinery maintenance

- US and Middle East exporters filling the gap, but with higher logistics costs

- Buyers increasingly lock in prices and secure long-term contracts to manage risk

9. Key Suppliers and Exporters

9.1. Middle East

The Middle East remains a dominant exporter of EN590 diesel, leveraging:

- Abundant crude reserves

- Advanced refining capacity (Saudi Arabia, UAE, Kuwait)

- Proximity to major sea routes and global shipping hubs

Middle Eastern refineries are investing in compliance upgrades to meet EN590 and other international standards.

9.2. Russia

Russian diesel exports have been curtailed by EU sanctions since 2022, with further tightening in 2025 targeting refined products processed in Türkiye and India. This has forced European buyers to diversify sources, increasing demand from the Middle East, US, and India.

9.3. United States

US Gulf Coast refineries are major exporters to Europe and Latin America, benefiting from flexible configurations and access to discounted domestic crude.

9.4. India

India is rapidly expanding its refining and export capacity, with IOC, BPCL, and Reliance leading large-scale projects targeting both domestic and international markets.

9.5. Africa

Nigeria’s Dangote refinery is transforming West and Central African supply, reducing import dependence and enabling exports to global markets.

10. Supply Chain Risks: Geopolitics, Shipping, and Logistics

10.1. Geopolitical Risks

Geopolitical complexity is the top challenge for energy companies in 2025, with risks including:

- Sanctions and trade restrictions (Russia, Iran, Venezuela)

- Conflicts affecting shipping routes (Red Sea, Suez Canal, Strait of Hormuz)

- Tariffs and regulatory fragmentation (US, EU, China)

Mitigation strategies:

- Diversify sourcing and logistics routes

- Build inventory buffers and flexible contracts

- Monitor regulatory developments and adapt compliance protocols

10.2. Shipping and Logistics

Shipping costs and risks are elevated due to:

- Volatile freight rates and insurance premiums

- Port congestion and infrastructure bottlenecks

- Weather-related disruptions and climate risks

Digitalization and supply chain visibility are becoming competitive advantages for exporters and traders.

11. Technological Advancements in Refining and Fuel Quality Testing

11.1. Refining Technology

Advances in hydroprocessing (e.g., IsoTherming®, deep HDS) enable efficient production of ULSD from a wider range of feedstocks, including LCO and heavy crudes.

Benefits:

- Lower operating costs and emissions

- Longer catalyst life and reduced maintenance

- Flexibility to meet evolving specifications

11.2. Fuel Quality Testing and Digitalization

Digital platforms and blockchain are enhancing:

- Traceability and documentation of fuel batches

- Real-time quality verification and compliance monitoring

- Shorter negotiation and contracting cycles

Independent laboratory testing and third-party certification are standard for high-value shipments.

12. Forecast Scenarios and Sensitivity Analysis

12.1. High, Medium, and Low Demand Scenarios

- Emerging markets (Asia, Africa) sustain rapid infrastructure and logistics growth

- Electrification and alternative fuels adoption slower than expected

- Geopolitical disruptions constrain supply, supporting higher prices

High Demand Scenario:

Medium (Base Case) Scenario:

- Moderate global growth, with Asia and Africa offsetting declines in Europe/North America

- Gradual adoption of biodiesel, HVO, and electrification in heavy-duty sectors

- Stable but competitive market, with regional rebalancing

Low Demand Scenario:

- Accelerated electrification and modal shifts in transport

- Aggressive policy interventions (urban diesel bans, carbon pricing)

- Rapid scale-up of renewable diesel and hydrogen, eroding diesel’s share

12.2. Sensitivity Factors

- Policy changes: Stricter emissions standards, blending mandates, or carbon taxes can accelerate demand shifts

- Technological breakthroughs: Cheaper batteries, hydrogen, or synthetic fuels could disrupt diesel’s dominance

- Geopolitical shocks: Supply disruptions or trade realignments can cause price spikes or shortages

13. Regional Comparison Table: Europe vs. Asia vs. Africa

Table 3: EN590 Diesel Market Comparison by Region (2026–2035)

| Factor | Europe | Asia (India, China, SE Asia) | Africa |

| Demand Trend | Flat/declining | Growing (esp. India, SE Asia) | Growing (esp. West, Central) |

| Regulatory Pressure | Very high (RED III, Green Deal) | Moderate to high (urban air quality) | Low to moderate |

| Refinery Capacity | Declining, import-dependent | Expanding (India, China) | Expanding (Dangote), but limited |

| Biodiesel Blending | B7–B10+, HVO, advanced biofuels | Limited, pilot projects | Minimal, some pilots |

| Alternative Fuels | HVO, e-diesel, electrification | LNG, hydrogen pilots, slow EV uptake | Early stage, focus on diesel |

| Import/Export Status | Net importer | Mixed (India: exporter; SE Asia: importer) | Net importer (except Nigeria) |

| Pricing Benchmarks | Rotterdam, ARA | Singapore, local indices | Linked to Europe, Middle East |

| Supply Chain Risks | Geopolitics, Russian sanctions | Feedstock, logistics, policy shifts | Infrastructure, FX, subsidies |

| Key Suppliers | Middle East, US, India, Africa | Middle East, India, China | Middle East, Dangote, Europe |

| Investment Focus | Renewable diesel, compliance | Refinery expansion, exports | Refinery upgrades, logistics |

Sources: Exporters Worlds, S&P Global, Data Insights Market, African Leadership Magazine, IOC, Dangote, ePURE, RED III, national policies

14. Implications for Refiners, Traders, and Distributors: Actionable Strategies

14.1. Refiners

- Invest in advanced hydroprocessing and blending infrastructure to meet evolving EN590 and renewable mandates

- Diversify product portfolios to include HVO, renewable diesel, and compliant blends

- Pursue digitalization for quality control, traceability, and supply chain optimization

14.2. Traders

- Prioritize compliance and documentation to access premium markets (Europe, regulated Asia)

- Leverage digital platforms for market intelligence, contract management, and risk mitigation

- Diversify sourcing and sales channels to manage geopolitical and supply chain risks

14.3. Distributors

- Secure long-term contracts with reliable suppliers to manage price and supply volatility

- Educate customers on compliance requirements and alternative fuel options

- Invest in storage and logistics to handle multiple grades and blends efficiently

15. Investment and Capex Trends in Refining and Renewable Diesel

- Major oil companies are allocating 42% of new capital to refinery upgrades for ULSD and renewable diesel production

- India, Middle East, and Africa are leading in new capacity and export-oriented investments

- Europe and North America are focusing on conversions to biofuels and compliance-driven upgrades

Email: exports@mketglobal.com

16. Data Sources and Market Intelligence to Monitor

Key benchmarks and agencies:

- Rotterdam/ARA, CME Group, S&P Global Platts: Price assessments for EN590 diesel

- National and regional agencies: IEA, Eurostat, BloombergNEF, African Leadership Magazine

- Industry platforms: Exporters Worlds, GGT Petrochemical, Neshes Global, GoGreen590Diesel

- Policy trackers: RED III, IMO, national biofuel mandates

Regular monitoring of these sources is essential for informed decision-making in a volatile and regulated market.

Conclusion: Navigating the EN590 Diesel Market in a Decade of Transition

The future demand for ULSD EN590 diesel will be defined by a delicate balance between enduring structural needs and accelerating energy transition pressures. While electrification and alternative fuels will erode diesel’s share in some segments and regions, EN590 diesel remains indispensable for heavy-duty transport, industrial activity, and economic growth in much of the world.

Success in the next decade will depend on:

- Compliance and traceability: Meeting ever-stricter standards and documentation requirements

- Technological adaptation: Investing in refinery upgrades, renewable blending, and digitalization

- Regional insight: Understanding the unique drivers, risks, and opportunities in each market

- Strategic agility: Diversifying supply chains, managing risk, and embracing innovation

For refiners, traders, and distributors, the EN590 diesel market is no longer about scale alone—it is about adaptability, credibility, and value-added service. Those who anticipate regulatory shifts, invest in cleaner technologies, and build resilient, transparent supply chains will be best positioned to thrive as the world’s energy landscape evolves.

Actionable Takeaways:

- Monitor regional policy and market intelligence for early signals of demand shifts and compliance changes

- Invest in advanced refining and blending technologies to future-proof operations

- Build long-term, transparent partnerships with buyers and suppliers, leveraging digital platforms for efficiency and trust

- Stay agile and diversified to navigate geopolitical, regulatory, and technological uncertainties